On every group tour I’ve ever done, one question that is always asked by the helpful customer service representative is whether or not I want to purchase travel insurance. These add-ons have become more popular over the years, and some tour companies will not allow you to travel to certain destinations without it. This topic will be a two part series. Today’s post (part 1) describes a brief overview of travel insurance, why you may want it, and why you may not want it. The second part to be published next week will discuss some general tips on acquiring it if you do decide to get some coverage.

There can be many, many components of travel insurance, but the following are the big ones:

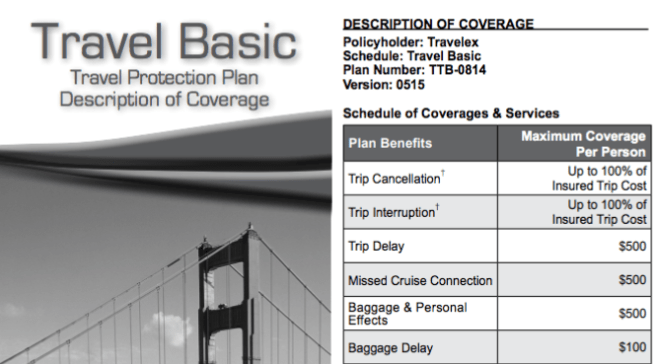

- Trip cancellation – reimburses your travel expenses in the event your trip gets cancelled, either by you for personal reasons or by the tour company. There’s a lot of fine print as to what does or does not get covered as a legitimate reason for cancellation.

- Trip interruption – covers the costs of returning home early while you’re in the middle of vacation.

- Medical protection – covers expenses if you get sick or injured. Like temporary health insurance.

- Medical evacuation – pays for the cost of transportation if you need to be airlifted to a different location for proper medical treatment.

- Baggage loss and delay – reimburses the cost of lost or damaged luggage; or if your bag shows up several days late, you’re covered for any essential items bought during the delay period.

- Accidental death – basically a life insurance policy if you die.

Before we delve into the details of the above components, I need to make clear my personal opinion on insurance in general.

The purpose of insurance is to protect oneself against financial catastrophe.

If a loss will not cause you great financial distress, then you do not need to insure against it. This is why we have health insurance; a few days’ stay in the ICU can easily run into the six figures and can absolutely wreck your financial life. Disability insurance replaces your income if you lose a hand in an accident and can’t work anymore. And term life insurance covers your loved ones in the event that you’re the main breadwinner and your family would have difficulty paying the bills if you died unexpectedly.

On the flip side, you do not need insurance on your iPhone. Or your TV. If you drop your phone in the middle of the street because you trip over a curb while texting and walking like a mindless tool, then you’re out your dignity and a few hundred dollars. But it is not a devastating life event. For me, small things like this are always self-insured, which means that instead of wasting my cash on unnecessary insurance over the course of my lifetime, I suck it up and pay out of pocket to repair or replace the item in the unlikely event that it breaks. How many times has this ever happened to me? Never. Not a single time. I know it will happen at some point, but by then I will have amassed a stockpile of cash to pay outright for a replacement device because instead of buying dozens of little insurance policies, I saved and invested that money instead.

When it comes to travel, losing a couple grand on a missed vacation really sucks, but it will not ruin you. Keep this in mind as we review the policy components.

Having said all of that, the most essential parts of travel insurance, if you choose to buy it, are medical protection and medical evacuation.

Health care is expensive, and it’s one of those things that can bankrupt you regardless of how well-off you are. All the other stuff is a pain in the ass if it happens, but it won’t make you destitute. You can eat the cost of a few thousand dollars on the rare chance that you have to cancel your plans at the last minute. You most certainly do not want to eat the cost of an emergency surgery and a 2 week hospital stay when you fall off of a zipline in South America.

Especially important if you are traveling someplace remote is the need for medical evacuation coverage. Getting airlifted on a private plane to a hospital in a different country is not cheap, so if you’re vacationing on a small island without full medical services, that one element is probably the most important type of coverage you want.

Now let’s go through the other components and I will try to convince you why you do not need to pay attention to anything other than medical coverage.

Trip cancellation – As mentioned above, this is not one of those life events that will wipe out your savings. In the unlikely scenario where you have to cancel your plans unexpectedly, then you accept the non-refundable expenses as a sunk cost and move on. In part 2 of this series, I’ll discuss Trip Cancellation insurance with actual numbers and show you why leaving out this one component leads to huge cost savings.

Trip interruption – Same reasons as trip cancellation. Don’t need it.

Baggage loss and delay – Come on man. You’re reading a blog about traveling the world with a backpack. Your bag will always be with you as a carry-on, and even if you do somehow lose your bag, there won’t be that much stuff in there, and all of it can be replaced. Skip it.

Accidental death – If this is really a concern, then you should have a proper term life insurance policy. Remember: Term Life. Never Whole Life. If anyone ever tries to sell you a Whole Life insurance policy, that person deserves a prompt punch in the face.

Keep in mind that it may not be possible to turn down specific components of travel insurance, but you can usually choose between different policies that have higher medical coverage and lower benefits for things like baggage loss and accidental death. It is always possible to decline trip cancellation coverage, and I’ll show you how to do that in part 2.

So far so good? Excellent. In part 2 of this topic, I’ll go over how to find a good travel insurance policy and how to get it for a decent price.