This post is a continuation of my Part 1 discussion of travel insurance. Today we’ll discuss whether or not you should even bother getting a travel insurance policy, and if you do decide you want one, how to go about acquiring it without getting ripped off.

Question 1: Do I even need to buy this?

If you’re young, in good shape, healthy, and going to a place that has a well-established health care system, then you probably don’t need travel insurance. Yes, something could happen; there’s always a small risk of that. But this is all about playing the odds. It is way less likely for a healthy 22 year old to have some kind of disaster on vacation compared to someone older with known chronic health problems. For young people, if you do get anything at all, it should only be medical coverage and medical evacuation, which you’ll see below is pretty cheap.

If you travel a lot, think about all the money you’ll be spending if you purchase travel insurance for every single one of your trips. If you go with full coverage, that adds up to a large amount of cash. Even if something does happen one time, you’ll likely still come out ahead financially by paying your expenses out of pocket compared to all the money you would have spent on insurance over the course of your lifetime.

Question 2: I’ve decided I want insurance. How do I go about getting it?

First of all, if you must buy travel insurance due to mandatory tour requirements — common for tours in Asia and other developing countries — then do not purchase it through the tour company. It is almost always sold at a marked up price (they’re making commission), and you can find better insurance policies for cheaper on your own.

The most important element of travel insurance is the company you purchase it from. You want to stick to big name, well established insurance companies. Look for those with an A.M. Best rating of either Superior or Excellent. It is not worth saving a few dollars to buy insurance from a no name po-dunk company that no one has ever heard of, because in the unlikely event that you actually need to use your policy, it is essential that you have a reputable firm that is ready to pay your claims. I have personally used Travelex and RoamRight in the past. AIG and Allianz are also some other big names.

The easiest way to compare quotes is to go to travelinsurance.com, fill in the boxes with your information, and it will spit out prices from several different reputable businesses.

You may want to also check with your credit card company to see if they provide some travel coverage. If the limits are sufficient, then you may not even need to buy additional coverage. Again, medical care and evacuation are the potential events that will make all your money disappear, so make sure those areas are covered well.

Question 3: Wow! This is expensive. How can I save some money and still have decent coverage?

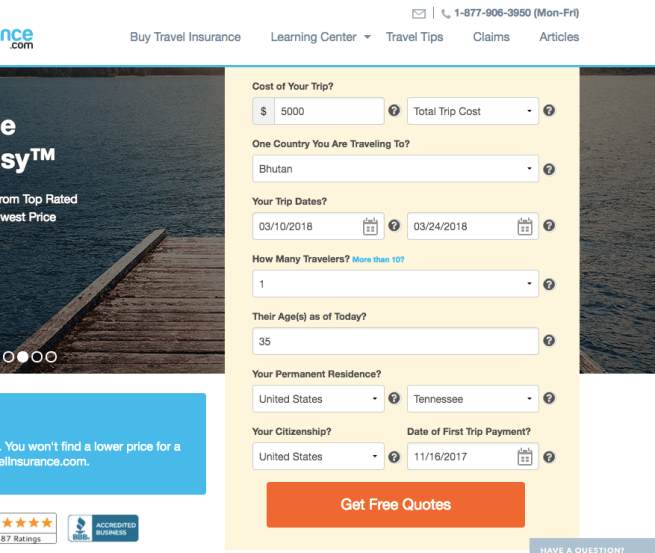

The most expensive part of travel insurance is trip cancellation. This is an add-on where if you have to cancel your vacation for whatever reason, the insurance company will reimburse you the entire nonrefundable cost of your expenses. Given that this is the most costly part of travel insurance, if you forego the trip cancellation portion, which I always have done in the past, the total cost of your policy will be a small fraction of the original price. The way you get rid of trip cancellation insurance, if there is no option to directly decline it, is to enter a zero in the box that says “Total Trip Cost.” Let’s plug in some numbers and see how much money we can save.

In the first example, let’s say we’re planning a solo 2 week trip to Bhutan, and the total trip costs are around $5000. We fill out all the boxes and click the box to see our free quotes:

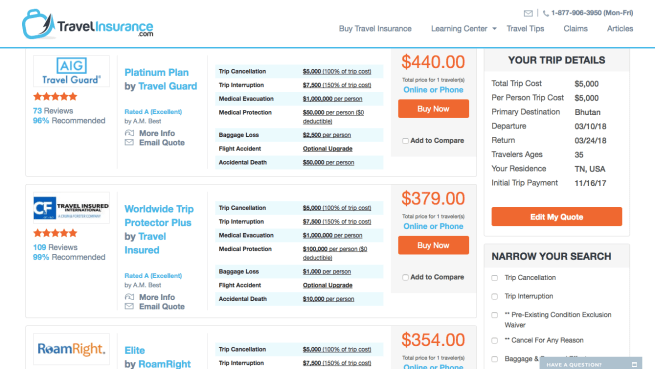

Okay. So we’re looking at around around $350 and up for full coverage policies. That’s a lot of cash.

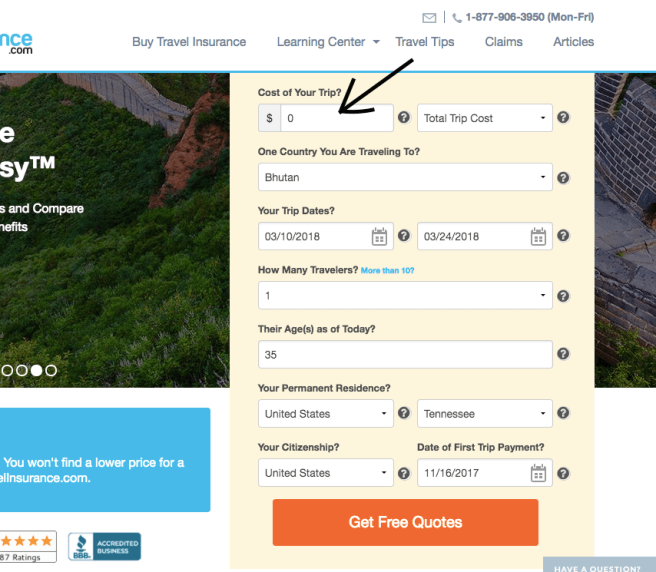

Now let’s get rid of the trip cancellation insurance and keep everything else the same. In the box labeled “cost of your trip”, type in a zero. In the screenshot below, it’s the box with the big black arrow pointing to it.

So now let’s submit this information and see what happens:

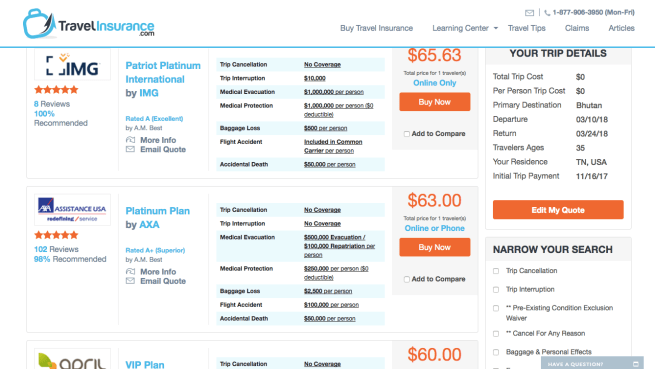

See the huge cost savings? By foregoing trip cancellation insurance, we’ve dropped the price of our insurance policy to 60 bucks; a fraction of the cost of our initial quote. By changing this one variable, we’ve reduced our insurance expense to 15% of the full coverage price, while still retaining the medical portion to cover rare but potentially devastating events.

Look again at the numbers above. The $65 IMG policy has a million dollars in both medical evacuation and medical protection. Pretty solid. The $440 AIG full policy only has a $50,000 limit on medical protection. If you end up in a hospital somewhere for a few days, that 50 grand can vanish in the blink of an eye. In this specific case, the cheaper $65 policy actually protects you better from the type of events that can really throw salt in your Kool-Aid.

So in summary, when considering travel insurance:

1) If you’re young and healthy, consider skipping it altogether

2) If you do buy it, don’t buy it from your tour company

3) Focus specifically on medical coverage and medical evacuation

4) Consider going without trip cancellation insurance to save a lot of cash

If any of you readers have ever been in an unfortunate circumstance where you needed to actually use your travel insurance while on vacation, I’d be curious to hear about your experiences.

I bought travel insurance from CSA travel Protection and Insurance Services a USA branch of Generali Assicurazioni Generali S.P.A. While on vacation, I needed to fly to Orlando, Florida to care for my hospitalized stepfather cancelling/interrupting my return flight to Los Angeles. The claim was denied due to my “non-traveling family member being DISCHARGED from hospital as there was no worsening of the condition while the coverage was in effect.” My claim was based on my stepfather being ADMITTED to the hospital, not DISCHARGED from hospital. My stepfather was admitted to hospital during the policy period covered which was my basis for claiming that my stepfather’s condition worsened. CSA and I did not reach an agreement despite numerous phone calls and written communication and supporting documentation. As was suggested in the letters of denial from CSA, I then filed a detailed complaint seeking assistance with suppporting documentation with the California Department of Insurance who contacted CSA and requested my claim be reevaluated. The CSA underwriter reviewed and reimbursed me for the costs to return home. I believe CSA chose not to honor their insurance contract until CSA was contacted by the California Department of Insurance. Perhaps the business model is to wear the claimant down so they will go away. As you know it is tedious and time consuming gathering documentation-copies of the hospital record, copies of tickets, phone calls, numerous written appeals, copies of the credit credit card payment of the tickets, copy of passport/driver license, followed by providing supporting documentation to the California Department of Insurance. I intended to file a lawsuit in Small Claims Court if the California Department of Insurance was unable to resolve my claim.

LikeLike

Glad to hear that you eventually got your claim resolved. Sounds like a pain to go through that entire process.

LikeLike